Published by: Sujan

Published date: 14 Jun 2021

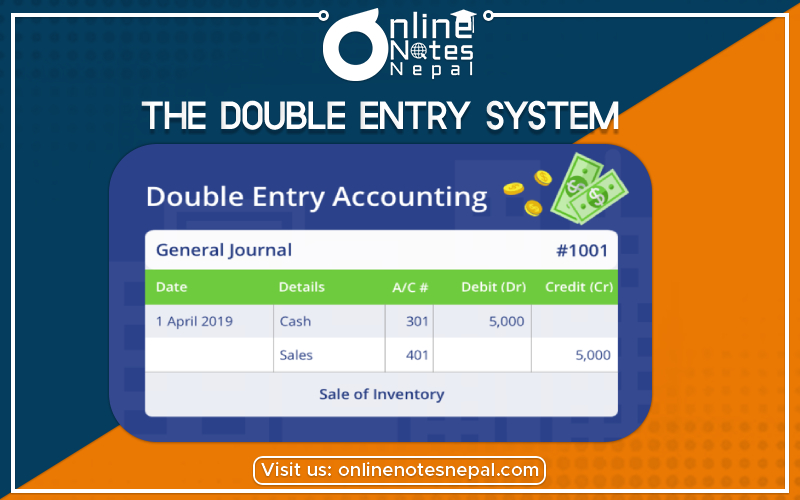

The double-entry system of accounting or bookkeeping means that for every business transaction, amounts must be recorded in a minimum of two accounts. The double-entry system also requires that for all transactions, the amounts entered as debits must be equal to the amounts entered as credits. It is a system of bookkeeping where every entry to an account requires a corresponding and opposite entry to a different account. The double-entry has two equal and corresponding sides known as debit and credit. The left-hand side is debit and the right-hand side is credit. It refers to an accounting concept whereby assets = liabilities + owners’ equity. In the double-entry system, transactions are recorded in terms of debits and credits.

Debits and credits are bookkeeping entries that balance each other out. Consider that for accounting purposes, every transaction must be exchanged for something else of the exact same value. To simplify this explanation, consider that a debit entry always adds a positive number and a credit entry always adds a negative number (even though positives and negatives are not used in the actual journal entries). For placement, a debit is always positioned on the left side of an entry (see chart below). A debit increases asset or expense accounts and decreases liability, revenue, or equity accounts.

A credit is always positioned on the right side of an entry. It increases liability, revenue, or equity accounts and decreases asset or expense accounts.

Debits and credits are used to record transactions in a company’s chart of accounts. A chart of accounts classifies income and expenses. The 5 major accounts are as follows:

ASSET ACCOUNT

Assets are items that provide future economic benefits to a company.

Examples of “Asset Account” subgroups include:

EXPENSE ACCOUNT

These are charges related to the day-to-day operation of a business.

Examples of “Expense Account” subgroups include:

REVENUE ACCOUNT

Revenue accounts are accounts related to income earned from the sale of products and services or interest from investments.

Examples of “Revenue Account” subgroups include:

LIABILITY ACCOUNT

Liabilities are obligations that the company is required to pay, such as vendor invoices.

Examples of “Liability Account” subgroups include:

EQUITY ACCOUNT

These are net asset entries (or the value of a company’s non-operational assets after liabilities have been paid).

Examples of “Equity Account” subgroups include: