Published by: Sujan

Published date: 14 Jun 2021

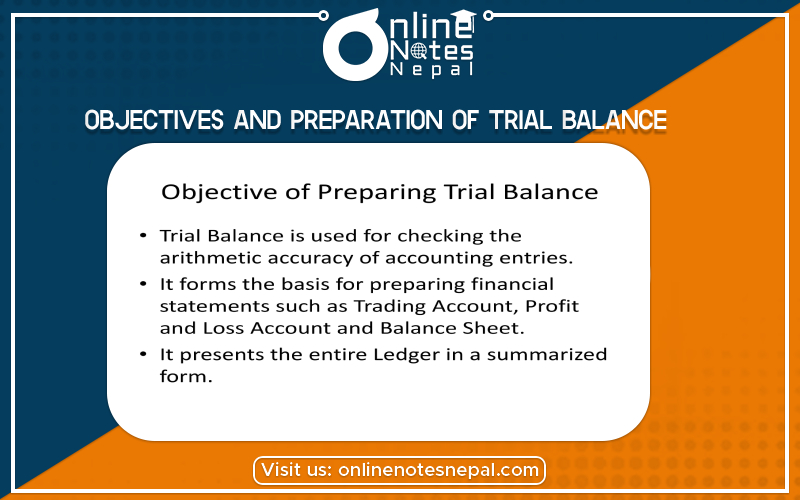

Objectives and Preparation of trial balance is a bookkeeping worksheet in which the balance of all ledgers is compiled into debit and credit account column totals that are equal. A company prepares a trial balance periodically, usually at the end of every reporting period. The general purpose of producing a trial balance is to ensure the entries in a company’s bookkeeping system are mathematically correct.

Objectives and Preparation of trial balance for a company serve to detect any mathematical errors that have occurred in the double-entry accounting system. If the total debits equal the total credits, the trial balance is considered to be balanced, and there should be no mathematical errors in the ledgers. However, this does not mean there are no errors in a company’s accounting system. For example, transactions classified improperly or those simply missing from the system could still be material accounting errors that would not be detected by the trial balance procedure.

One of the main objectives of the trial balance is to ensure that the total of all debits equals the total of all the credits. Preparing the trial balance is the third step of the accounting process. After journalizing and posting all entries in the ledgers, the bookkeepers prepare the trial balance. In the double-entry system of accounting, debit is always equal to credit. This means every individual account is perfectly matched. It also means that all accounts of the entity must match perfectly. One way to check this accuracy is through the Trial Balance of the company.

The first step in the preparation of final accounts is the preparation of the trial balance. So it is absolutely essential that we prepare the trial balance perfectly, so our final accounts do not contain any errors. Let us learn more about the methods and procedures of preparation of trial balance. Preparation of trial balance is the third step in the accounting process. First, we record the transactions in the journal. And then we post them in the general ledger. Then we prepare a trial balance to verify that the debit totals equal to the credit totals.

Let us take a look at the steps in the preparation of the trial balance.