Published by: Sujan

Published date: 14 Jun 2021

Preparation of adjusted trial balance is prepared by creating a series of journal entries that are designed to account for any transactions that have not yet been completed. These items include payroll expenses, prepaid expenses, and depreciation expenses. Preparing an adjusted trial balance is the sixth step in the accounting cycle. An adjusted trial balance is prepared by creating a series of journal entries that are designed to account for any transactions that have not yet been completed.

These items include payroll expenses, prepaid expenses, and depreciation expenses. Here are the steps used to prepare an adjusted trial balance:

To understand what an adjusted trial balance is, we first have to view an unadjusted trial balance as well as the necessary journal entries to complete in order to prepare an adjusted trial balance.

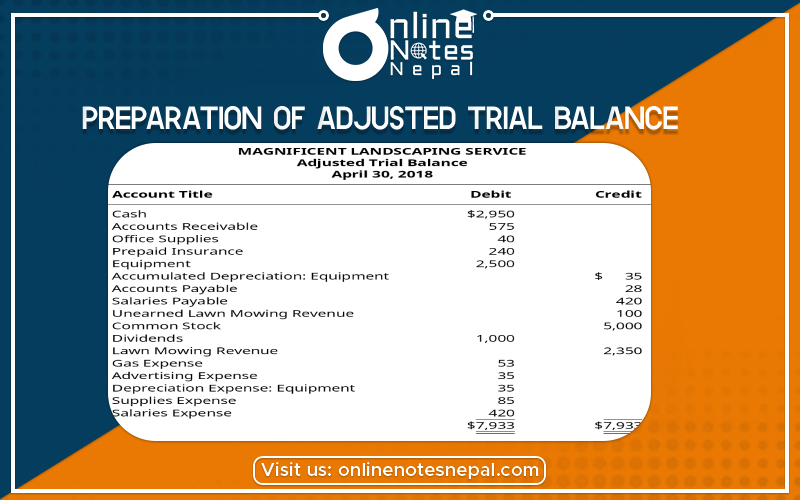

Step 1: Run an unadjusted trial balance

Step 2: Enter adjusting journal entries

Step 3: Run an adjusted trial balance

Before posting any closing entries, you want to make sure that your trial balance reflects the most accurate information possible.

Both the unadjusted trial balance and the adjusted trial balance play an important role in ensuring that all of your accounts are in balance and financial statements will reflect the most accurate totals.

What is the purpose of an adjusted trial balance?

An adjusted trial balance provides you with the summary totals of all of your general ledger accounts after adjusting entries have been made.

What relation does an adjusted trial balance have to the general ledger?

Both the unadjusted and the adjusted trial balance are listings of the ending balances of all of your general ledger accounts.

What entries are typically made to the adjusted trial balance?

Adjusting entries typically include payroll accruals, prepayment adjustments, and depreciation expenses that have not yet been recorded.