Published by: Sujan

Published date: 14 Jun 2021

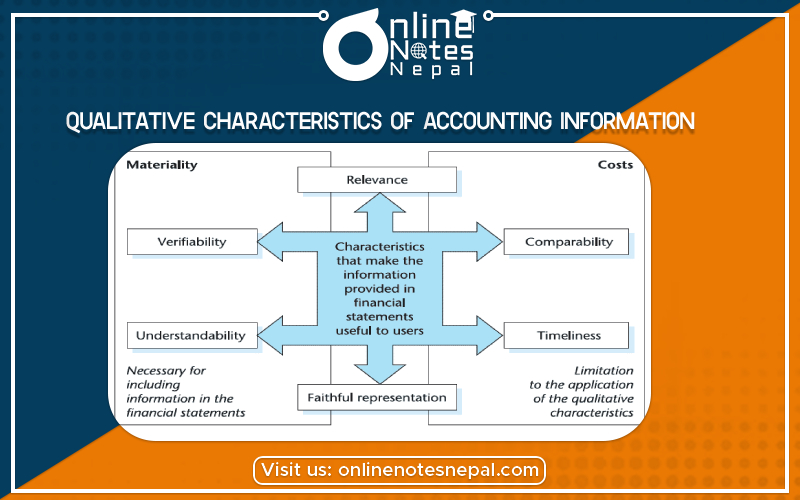

Following are the points regarding the qualitative characteristics of accounting information.

For anything to be useful, it must be understandable. Usefulness and understandability go hand in hand. However, the understandability of financial information varies considerably, depending on the background of the user. The financial information should be comprehensible to those who are willing to spend time to understand it.

To be relevant to investors, creditors, and others for investment, credit, and similar decisions, accounting information must be capable of making a difference in a decision. Relevant information should have the following values.

Accounting information is reliable to the extent that users can depend on it to represent the economic conditions or events that it purports to represent. Reliability has three basic characteristics:

Qualitative Accounting information about an enterprise is extremely useful if it can be compared to accounting information about other enterprises. Comparability results when different enterprises apply the same accounting treatment to similar events. Comparability results when different enterprises apply the same accounting treatment to similar events. Compliance with international accounting standards helps to enhance comparability.

Consistency means conformity from period to period with unchanging policies and procedures. COnformity can be achieved by applying the same accounting treatment to similar events from period to period. It does not mean that an enterprise can’t switch from one accounting method to another if the new method is justified and is preferable. The enterprise should disclose the reasons and the effect of such a change.

Materiality is the magnitude of an accounting information omission or misstatement that will affect the judgment of someone relying on the information. According to this feature, not all the financial matters are to be reported which have no significant impact on decision making and only the material information is to be disclosed.

The practice of using the least optimistic estimate when two estimates of amounts are about equally likely. Conservation means a tendency to play safely while presenting the information through financial statements. Accounting to which all the possible expenses/losses are anticipated but all possible incomes/gains are not anticipated which are likely to happen in future to determine the profit or loss.

Most decision-makers assume that information is a cost-free commodity, while providers know it is not. The costs of providing the information should be weighed against the benefits of using the information. Cost-benefit decisions are extremely difficult because both costs and benefits are often subjective and difficult or impossible to measure reliably.