Published by: Sujan

Published date: 14 Jun 2021

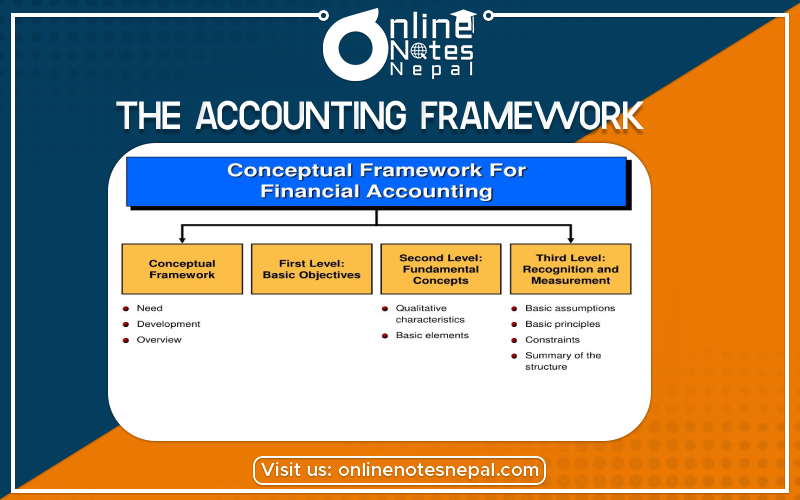

An accounting framework is a published set of criteria that is used to measure, recognize, present, and disclose the information appearing in an entity’s financial statements. An organization’s financial statements must have been constructed using a recognized framework, or else auditors will not issue a clean audit opinion for them. The theoretical framework of Accounting refers to the set of frameworks, methods, and assumptions used in the study and application of accounts in financial situations.

Accounting assumptions state how a business is organized and operates. They provide structure to how business transactions are recorded. If any of these assumptions are not true, it may be necessary to alter the financial information produced by a business and reported in its financial statements. These assumptions are:

Generally accepted accounting principles (GAAP) refer to a common set of accounting principles, standards, and procedures issued by the Financial Accounting Standards Board (FASB). Public companies in the United States must follow GAAP when their accountants compile their financial statements. GAAP is a combination of authoritative standards (set by policy boards) and the commonly accepted ways of recording and reporting accounting information. GAAP aims to improve the clarity, consistency, and comparability of the communication of financial information. GAAP helps govern the world of accounting according to general rules and guidelines. It attempts to standardize and regulate the definitions, assumptions, and methods used in accounting across all industries. GAAP covers such topics as revenue recognition, balance sheet classification, and materiality.

An accounting Information System is software that a business uses in collecting, storing, and processing financial data that are used for decision-making. To simplify, Accounting Information System gives accurate data to the managers before making any significant decisions that will either make or break their business. The purpose of an accounting information system (AIS) is to collect, store, and process financial and accounting data and produce informational reports that managers or other interested parties can use to make business decisions.

Development of AIS includes five basic phases: