Published by: Sujan

Published date: 14 Jun 2021

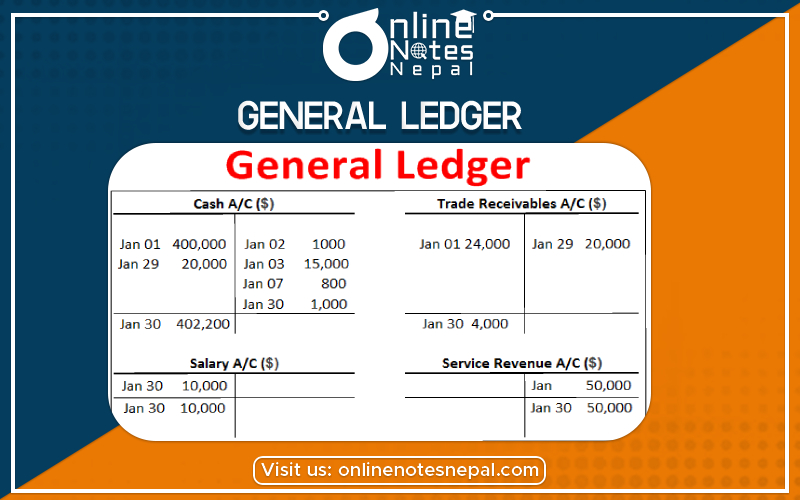

A general ledger is the foundation of a system used by accountants to store and organize financial data used to create the firm’s financial statements. Transactions are posted to individual sub-ledger accounts, as defined by the company’s chart of accounts. In bookkeeping, a general ledger, also known as a nominal ledger, is a bookkeeping ledger in which accounting data is posted from journals and from sub-ledgers, such as accounts payable, accounts receivable, cash management, fixed assets, purchasing, and projects.

The general ledger contains a debit and credit entry for every transaction recorded within it so that the total of all debit balances in the general ledger should always match the total of all credit balances. If they do not match, the general ledger is said to be out of balance and must be corrected before reliable financial statements can be compiled from it.

The general ledger is comprised of all the individual accounts needed to record the assets, liabilities, equity, revenue, expense, gain, and loss transactions of a business. In most cases, detailed transactions are recorded directly in these general ledger accounts. In some cases where the volume of transactions would overwhelm the record-keeping in the general ledger, transactions are shunted off to a subsidiary ledger, from which just the account totals are recorded in a control account in the general ledger. In the latter case, a person researching an issue in the financial statements must refer back to the subsidiary ledger to find information about the original transaction. The general ledger is usually printed and stored in an organization’s year-end book, which serves as the annual archive of its business transactions.

Some of the more common balance sheet accounts and how they are further arranged in the general ledger include:

Some general ledger accounts can become summary records and will be referred to as control accounts. In that situation, all of the detail that supports the summary amounts in one of the control accounts will be available in a subsidiary ledger.

Examples of General Ledger Control Accounts

A common example of a general ledger account that can become a control account is Accounts Receivable. The summary amounts are found in the Accounts Receivable control account and the details for each customer’s credit activity will be contained in the Accounts Receivable subsidiary ledger.

Other general ledger accounts that may become control accounts include Inventory, Equipment, and Accounts Payable.