Published by: Sujan

Published date: 14 Jun 2021

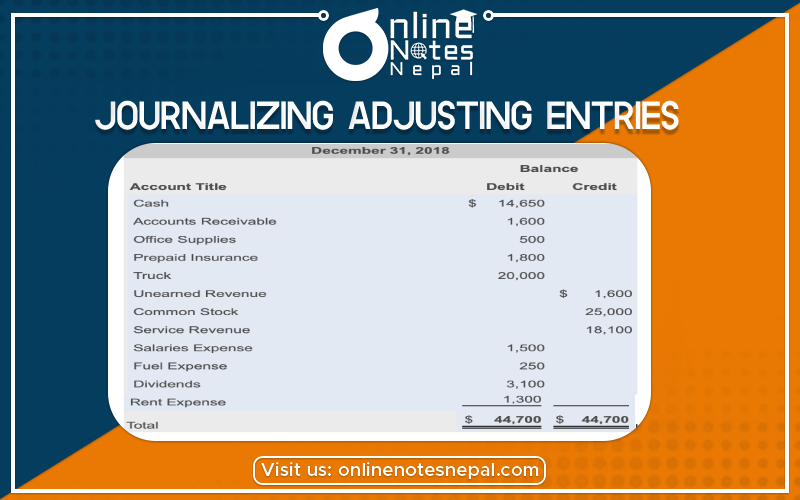

Journalizing adjusting entries are made in your accounting journals at the end of an accounting period after a trial balance is prepared. After adjusting entries are made in your accounting journals. They are posted to the general ledger in the same way as any other accounting journal entry. There are several types of adjusting entries that can be made, with each being dependent on the type of financial activities that define your business.

Adjusting entries are necessary to update all account balances before financial statements can be prepared. … The accountant examines a current listing of accounts—known as a trial balance—to identify amounts that need to be changed prior to the preparation of financial statements.

The purpose of adjusting entries is to accurately assign revenues and expenses to the accounting period in which they occurred.

Whenever you record your accounting journal transactions, they should be done in real-time. If you’re using an accrual accounting system, money doesn’t necessarily change hands at that time of the accounting entry; the purpose of adjusting entries is to show when the money was officially transferred and to convert your real-time entries to entries that accurately reflect your accrual accounting system.

An adjusting entry can be used for any type of accounting transaction; here are some of the more common ones:

Journalizing adjusting journal entries are accounting journal entries that update the accounts at the end of an accounting period. Each entry impacts at least one income statement account (a revenue or expense account) and one balance sheet account (an asset-liability account) but never impacts cash.

Adjustments entries fall under five categories: accrued revenues, accrued expenses, unearned revenues, prepaid expenses, and depreciation.