Published by: Dikshya

Published date: 05 Jul 2023

- The determination of the equilibrium level of income in a two-, three-, or four-sector economy is based on the concept of aggregate demand and aggregate supply. The sectors in these economies represent different components of expenditure or income generation.

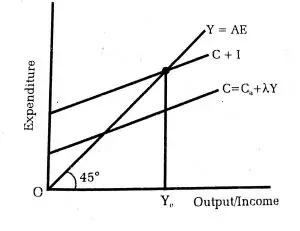

- In a two-sector economy, there are two main sectors: households and firms. The equilibrium level of income is determined by the equality of aggregate demand (AD) and aggregate supply (AS) within these two sectors.

Aggregate Demand (AD): In a two-sector economy, aggregate demand consists solely of household consumption (C). It represents the total amount of goods and services that households are willing and able to purchase at different levels of income.

Aggregate Supply (AS): Aggregate supply is determined by the total production or output (Y) of the firms in the economy. It represents the total quantity of goods and services that firms are willing and able to produce at different levels of income.

Equilibrium Level of Income: The equilibrium level of income occurs when aggregate demand equals aggregate supply. Mathematically, Y = C. At this equilibrium point, total output is equal to total consumption.

The equilibrium level of income can be illustrated graphically using a 45-degree line diagram. In this diagram, the horizontal axis represents income (Y), and the vertical axis represents aggregate demand (AD) and  aggregate supply (AS). The 45-degree line represents the equilibrium level of income, where AD is equal to AS. The intersection point of the AD curve and the 45-degree line represents the equilibrium level of income. At this point, the quantity of goods and services demanded by households is equal to the quantity supplied by firms.

aggregate supply (AS). The 45-degree line represents the equilibrium level of income, where AD is equal to AS. The intersection point of the AD curve and the 45-degree line represents the equilibrium level of income. At this point, the quantity of goods and services demanded by households is equal to the quantity supplied by firms.

Any deviation from the equilibrium level of income will create imbalances in the economy. If aggregate demand exceeds aggregate supply, it results in a situation of excess demand, leading to rising prices and increased production. On the other hand, if aggregate supply exceeds aggregate demand, it results in a situation of excess supply, leading to falling prices and reduced production. The determination of the equilibrium level of income in a two-sector economy simplifies the analysis by considering only household consumption and firm production. It provides a foundational understanding of the relationship between spending and production in an economy.

- IIn a three-sector economy, the three main sectors are households, firms, and the government. The equilibrium level of income is determined by the equality of aggregate demand (AD) and aggregate supply (AS), taking into account consumption, investment, government expenditure, and savings.

Aggregate Demand (AD): In a three-sector economy, aggregate demand consists of three components:

Household Consumption (C): This represents the total spending by households on goods and services. It is influenced by factors such as disposable income, consumer confidence, and interest rates.

Investment (I): Investment represents the spending by firms on capital goods, such as machinery, equipment, and construction. It is influenced by factors such as interest rates, business expectations, and technological advancements.

Government Expenditure (G): Government expenditure includes spending by the government on goods and services, such as infrastructure, defense, healthcare, and education. It is determined by government policies, budget allocations, and economic objectives.

Aggregate Demand Equation: AD = C + I + G

Aggregate Supply (AS): Aggregate supply is determined by the total production or output (Y) of the firms in the economy. It represents the total quantity of goods and services that firms are willing and able to produce at different levels of income.

Equilibrium Level of Income: The equilibrium level of income occurs when aggregate demand equals aggregate supply. Mathematically, Y = C + I + G. At this equilibrium point, total output is equal to total spending by households, firms, and the government. The equilibrium level of income can be graphically represented by plotting the aggregate demand (AD) and aggregate supply (AS) curves on a graph, with the vertical axis representing income (Y) and the horizontal axis representing aggregate expenditure.

The equilibrium level of income is reached at the intersection point of the AD and AS curves. At this point, total spending (AD) is equal to total output (AS), indicating that the economy is in balance. It's important to note that in a three-sector economy, saving (S) is implicitly assumed to be equal to investment (I). This assumption implies that all savings are channeled into investment in the economy, maintaining the equilibrium level of income. Understanding the equilibrium level of income in a three-sector economy helps in analyzing the relationships between consumption, investment, government expenditure, and overall economic activity.

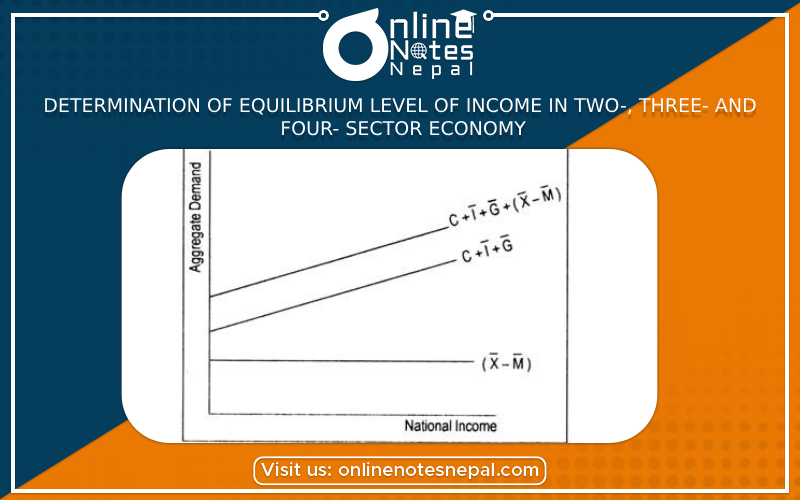

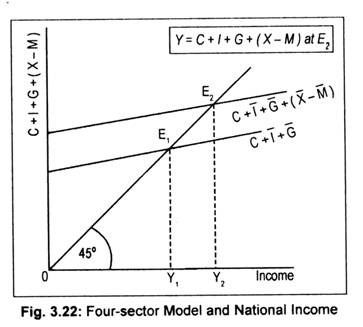

In a four-sector economy, there are four main sectors: households, firms, government, and the foreign sector (exports and imports). The equilibrium level of income is determined by the equality of aggregate demand (AD) and aggregate supply (AS) within these sectors, taking into account consumption, government expenditure, savings, and net exports.

Aggregate Demand (AD): In a four-sector economy, aggregate demand consists of household consumption (C), government expenditure (G), savings (S), and net exports (exports - imports). AD = C + G + S + (X - M), where X represents exports and M represents imports.

Aggregate Supply (AS): Aggregate supply is determined by the total production or output (Y) of the firms in the economy.

Equilibrium Level of Income: The equilibrium level of income occurs when aggregate demand equals aggregate supply. Mathematically, Y = C + G + S + (X - M). At this equilibrium point, total output is equal to to tal consumption, government expenditure, savings, and net exports.

tal consumption, government expenditure, savings, and net exports.

To understand the determination of the equilibrium level of income in a four-sector economy, we can use a basic model known as the Keynesian cross. This model depicts the relationship between aggregate demand and aggregate supply. In the Keynesian cross diagram, the horizontal axis represents income (Y), and the vertical axis represents aggregate demand (AD) and aggregate supply (AS). The AD curve is formed by the sum of consumption, government expenditure, savings, and net exports. The AS curve represents the total production or output (Y) generated by the firms in the economy. The equilibrium level of income is determined by the point of intersection between the AD and AS curves. At this point, aggregate demand is equal to aggregate supply, ensuring a balance in the economy. If aggregate demand exceeds aggregate supply, there is excess demand, which can lead to rising prices and increased production to meet the demand. Conversely, if aggregate supply exceeds aggregate demand, there is excess supply, which can result in falling prices and reduced production.

In summary, the equilibrium level of income in a four-sector economy is determined by the equality of aggregate demand and aggregate supply, considering consumption, government expenditure, savings, and net exports. The interplay between these sectors influences the overall level of economic activity and stability.